Q3 Economic and Financial Market Outlook

July 20, 2023

By: Peter R. Phillips, CFA®, CAIA®

Senior Vice President and Chief Investment Officer

Washington Trust Wealth Management

With the economy and markets performing far better than expected through Q2, there are some reasons to be optimistic... but many reasons to remain cautious.

Q2 and YTD Recap: Resilience Despite Headwinds

The U.S. economy and financial markets remained resilient despite significant headwinds. First quarter U.S. GDP growth of 2.0% was much better than the slightly negative growth rate expected as we entered 2023.i The labor market remained quite strong, which along with still pent-up savings and demand from the pandemic, helped drive consumer spending. Positive economic momentum likely carried into the just-finished second quarter, as suggested by the Atlanta Fed’s GDPNow estimate of 2.1%.ii

Stock prices rallied, with the S&P 500 producing a total return of 8.7% for the quarter and 16.9% YTD.iii Excitement related to the Artificial Intelligence (AI) investment theme helped stock prices. Fixed income returns were under pressure in the quarter but remained positive YTD. The Bloomberg U.S. Aggregate Index was down 0.8% in the quarter due to an increase in market interest rates but is up 2.1% YTD.iv

Significant headwinds

This resilience is both impressive and surprising, considering several significant headwinds. The Fed continued on its hawkish (restrictive) policy path, with a 25bp Fed funds rate increase in May—on top of 475bp of gains since March of 2022—the fastest and most significant Fed Funds rate increase since 1980.v The banking industry was pressured by three of the largest bank failures in U.S. history. And the U.S. debt ceiling crisis, while resolved for the near term, created angst amongst investors and highlighted the somewhat precarious condition of the country’s finances.

Economic Outlook: Still Cautious

While economic growth in the first half of 2023 was far better than expected, it does not change our cautious outlook on the economy. There remain too many indicators suggesting a cautious outlook is warranted.

More Fed Impact

The Fed’s restrictive monetary policy stance continues to cloud the economic outlook. We are witnessing the fastest rate increase since 1980, with increases totaling 500bp in 15 months and another 50bp being projected.vi Further, the Fed funds futures market does not expect a pivot to a more accommodative policy until mid-2024. The impact of monetary policy involves “long and variable lags” that can take 9 to 24 months to impact the economy.vii Past Fed fund rate increase cycles have led to a slowdown in economic growth and often recession.

Inverted U.S. Treasury Yield Curve

The inverted U.S. Treasury yield curve we are experiencing has historically been a strong indicator of recession. Both the 2y – 10y U.S. Treasury spread and 3m – 10y U.S. Treasury spread were decidedly inverted on June 30, 2023 (at -106bp and -150bp, respectively) and have been so for an extended period. The Federal Reserve Bank of New York’s recession probability indicator, based on U.S. Treasury yield spreads, puts the probability of recession within the next twelve months at 67%.viii

Banking Industry Woesix

Although fallout from bank failures earlier in the year appears to have been contained, and results of the Fed’s recent annual stress test on the country’s largest banks suggest these banks are sufficiently capitalized,x operating conditions remain challenging for the banking industry. Deposits continue to flow out of banks into competing, higher-yielding products. Total deposits declined $472.1 billion in the first quarter, the fourth quarter in a row of deposit outflow, and the largest quarterly decline since 1984, when data collection began. We anticipate outflows continued in the second quarter and will likely persist for the balance of the year. Banks need to replace these lost deposits with higher-cost funding, which hurts profitability.

Deposit outflows also present potential liquidity challenges.

Banks also continue to hold significant unrealized investment losses in their investment securities portfolios. As of March 31, 2023, this amounted to $515 billion, or 23% of bank equity capital. Market interest rates have trended higher since March 31, which has not likely helped improve these loss levels in Q2, recognizing that the price/value of a bond moves inversely with the direction of interest rates. The combination of banks’ higher borrowing costs and reduced liquidity could serve to further tighten bank lending standards, which are already at levels historically associated with economic slowdown and recession.xi

The combination of banks’ higher borrowing costs and reduced liquidity could serve to further tighten bank lending standards, which are already at levels historically associated with economic slowdown and recession.

U.S. Government’s Fiscal Health

We are also a bit concerned about the U.S. government’s fiscal condition and its potential to negatively impact government spending and tax policy, and in turn, economic growth in the years to come. The gross debt of the United States government has grown $9.1 trillion, or 39% since the end of 2019 (just before the pandemic). It now stands at $32.3 trillion (as of 6/30/23).xii Due to the significantly higher debt levels and the sharp rise in interest rates over the past year, the Congressional Budget Office (CBO) estimates that net interest payment on the nation’s debt (or the cost just to service the debt) will rise to over 15% of total government revenue by 2025, up from 9.7% in 2022, and an average of 8.7% from 2013-2022. This has significant implications for government spending and tax policy in the years to come, especially given that the U.S. budget already operates in a deficit, which the CBO estimates to be approximately 18% of revenue in 2023.xiii

More Indicators

Various other economic indicators also suggest caution is warranted. The Conference Board Leading Economic Index (LEI), which includes ten components across financial, labor, manufacturing, consumer, and housing markets, has declined in each of the last fourteen months and is at a level that signals recession within the next 12 months.xiv The Institute for Supply Management (ISM) index of manufacturing activity has been weakening and suggesting economic contraction since late 2022, with the new orders and backlog components of the index especially weak.xv Consumer confidence levels have fallen, especially the future expectations component, which is at levels typically associated with recession.xvi

Recession Outlook

A cautious outlook does not mean a recession is inevitable. An economic “soft-landing” is certainly possible.xvii

Strong U.S. Labor Market

The U.S. labor market continues to generate strong new job growth. An additional 1.7 million jobs have been created through the first half of 2023 and the unemployment rate of 3.6% remains near historic low levels.xviii While the pace of monthly job growth is moderating, it remains above pre-pandemic levels and is across most segments of the economy.

Consumer Spending

The robust employment landscape has resulted in good personal income gains. Real (after adjustments for inflation) disposable personal income is improving and grew a robust 4.4% over the past year.xix Good personal income gains have resulted in continued consumer spending. Real personal consumption expenditures are growing at a relatively solid 2% pace.

Easing Inflation

Further, inflation pressures continue to moderate, which may allow the Fed to end its tightening cycle. The Consumer Price Index (CPI) rose 3.1% on a year-over-year basis for the period ended June 30, 2023, the lowest level since March 2021. For the same period, “Core” CPI, which excludes volatile food and energy prices, rose 4.9%, still a bit high but trending lower and the lowest level since October 2021. While both CPI measures are above the Fed’s 2% target, expectations are for inflation to continue to moderate. With inflation in check, the Fed may be in a position to pause Fed funds rate increases—and potentially move to a more accommodative monetary policy position, which would be viewed as a positive for both the economy and financial markets.

Soft Landing

The FactSet consensus estimate for U.S. GDP growth suggests a soft landing. The U.S GDP growth slowdown originally expected in early-to-mid 2023 has been pushed out to late 2023/early 2024. The FactSet consensus 2023 U.S. GDP growth estimate is 1.1%, up significantly from the 0.3% estimate at the beginning of the year. The FactSet consensus 2024 U.S. GDP growth estimate is 0.7%, down significantly from the 1.3% estimate at the beginning of the year. However, quarterly U.S. GDP growth estimates now call for only one-quarter of slightly negative growth in Q4, versus beginning-of-year expectations for two consecutive quarters of negative growth. Recessions are typically defined as at least two consecutive quarters of negative GDP growth.[xx] In general, while both 2023 and 2024 GDP growth estimates remain quite low, current estimates suggest the economy will avoid a deep and protracted recession.

While both 2023 and 2024 GDP growth estimates remain quite low, current estimates suggest the economy will avoid a deep and protracted recession.

Financial Markets

In general, we maintain our near-term cautious outlook for both the equity and fixed-income markets but see an opportunity to get more constructive as we go through 2023. Near-term uncertainty on Fed policy, the banking industry, and the trajectory of the U.S. economy are some of the factors that make it difficult to have high conviction that it will be all smooth sailing for the markets over the coming months and quarters.

Fixed Income

The large increase in yields over the past year surely makes fixed income investments more attractive, and it is probably a good time to add some duration to portfolios, with a continued preference for high quality.

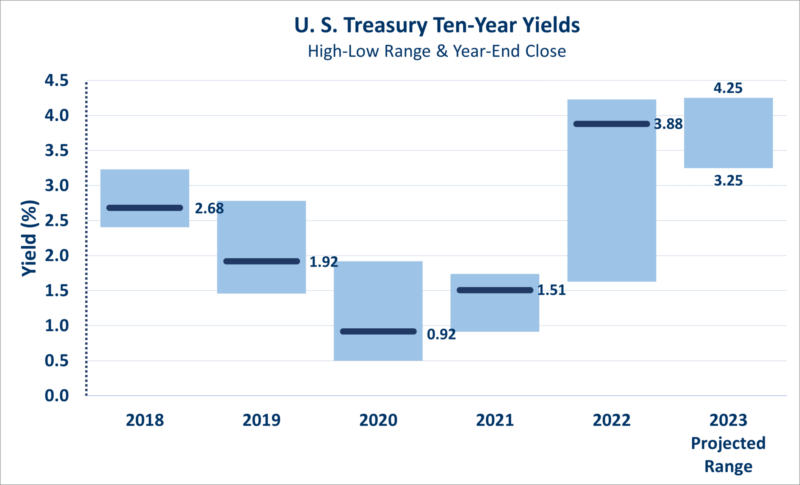

Portfolio Duration. The 2-year Treasury ended the quarter yielding 4.87%, up sharply from 4.06% at the end of the first quarter and close to the 15+ year high of 5.06% achieved in early March. The 10-year Treasury ended the quarter yielding 3.81%, up from 3.49% at the end of the first quarter. While a bit below the one-year high of 4.23%, 3.81% is still close to the highest yields in about twelve years.xxi

Yields could continue to trend upward, given still higher-than-target inflation levels and expectations for additional Fed funds rate increases. Conversely, an economic slowdown and/or recession would likely reduce Fed fund rate expectations and also create a “flight to quality,” both of which would likely result in lower bond yields and positive returns for fixed income investments.

Trying to time the exact inflection point of peak yields is probably not the best investment strategy. With yields near 12–15-year highs and still elevated recession risk, it likely makes sense to add some duration to portfolios and lock in some higher yields for the longer term.

Current high money market yields are likely to fall should the Fed pause and pivot.

Credit Spreads. Given the still high probability of recession and likely widening credit spreads, it may be too early to add exposure to lower-quality corporate bonds and other higher-risk, credit-sensitive segments of the fixed-income market. Investment grade spreads at 123bp remain slightly below the twenty-year average of about 149 bp and significantly below spreads during economic slowdowns and recessions. High Yield spreads at 390bp remain significantly below the 20-year average of about 496bp, and significantly below spreads during economic slowdowns and recessions.

U.S. Equity

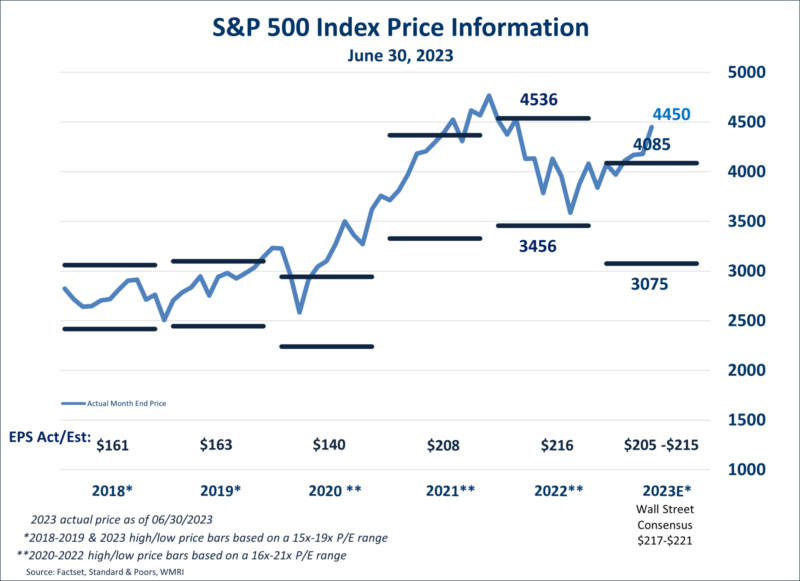

We certainly like higher stock prices; however, the recent rally in equity prices appears a bit disconnected from underlying trends in the economy and corporate earnings, as well as the relatively high inflationary and interest rate environment. Stocks do not appear “cheap”, and we expect earnings estimates to fall. As such, we continue to have a cautious outlook for stock prices.

Corporate Earnings. Corporate earnings estimates appear too high and not consistent with economists’ consensus forecast for an economic slowdown and/or recession. Current consensus S&P 500 earnings call for 2023 earnings growth of 1.0% and 2024 growth of 11.6%; however, economic slowdowns and recessions typically result in EPS (earnings per share) declines. The median EPS decline during recession is 22%.xxii

Valuation. The rally in stock prices so far this year puts the current S&P 500 price/earnings ratio (valuation) based on 2023 estimates at 20.2x. This is not a cheap valuation, especially in a high inflationary and interest rate environment. If inflation fails to subside in the coming year, then we see a downside risk to valuation. There is an inverse correlation between inflation and p/e ratios; higher inflationary environments typically result in lower p/e ratios. Current valuation levels leave little room for any disappointment, whether it be from the economy, corporate earnings, or some other unforeseen risk.

Artificial Intelligence (AI) Investment Theme. To be sure, a small subset of mostly information technology stocks with exciting growth potential related to artificial intelligence (AI) technologies account for an extremely large portion of the S&P 500’s performance year-to-date.xxiii We share the enthusiasm for the potential of AI to transform our lives and businesses across many industries; however, recent stock price strength may be a bit premature.

International Equity

We continue to underweight our exposure to international equities but see performance benefits from a weak U.S. dollar.

Although valuations appear significantly lower than in the U.S., earnings growth rates across the developed international countries are much less attractive, partly due to their more modest exposure to global-scale information and medical technology companies. In addition, the Russian/Ukraine conflict has a much greater and direct impact on economies across Europe. Recession risk is elevated across Europe. In the emerging markets, heightened risks keep us cautious—specifically, geopolitical risks related to China.

We would expect a weaker U.S. dollar to boost unhedged international investment returns. The U.S. dollar fell 2.2% versus the Euro year-to-date and has fallen 13.4% from the high reached in September 2022.xxiv Consensus forecasts call for further dollar weakness in anticipation of lower U.S. inflation, a more neutral-to-accommodative U.S. Federal Reserve policy, and improving global economic growth relative to the U.S. As such, we do see value in having some exposure to international equities.

Long Term Perspective

While our near-term outlook remains one of caution, it is important to remain focused on a long-term financial plan and investment strategy. If you have questions about how the market and economy are impacting your portfolio, your Washington Trust team is here to help.

i - Actual 1q:23 results from Bureau of Economic Analysis, 1Q:23 GPD (third estimate) news release, June 29, 2023. Expected growth rate data from Factset.

ii - Federal Reserve Bank of Atlanta, 2q:23 GDPNow estimate, July 6, 2023

iii - Factset

iv - Factset

v - Federal Reserve, Factset

vi - Federal Reserve, FOMC Summary of Economic Projections, June 14, 2023

vii - Federal Reserve Bank of St. Louis, “Examining Long and Variable Lags in Monetary Policy’, Bill Dupor, May 24, 2023.

viii - FactSet, Federal Reserve Bank of New York

ix - Bank industry data from the FDIC Quarterly Banking Profile, First Quarter 2023

x - Board of Governors of the Federal Reserve System, 2023 Federal Stress Test Results, June 2023

xi - Factset, Federal Reserve, April 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices

xii - U.S Department of the Treasury. Fiscaldata.treasury.gov

xiii - Congressional Budget Office. An Update to the Budget Outlook: 2023 to 2033, May 2023

xiv - The Conference Board, US Leading Indicators press release, June 22, 2023

xv - Factset

xvi - Factset

xvii - A ‘soft-landing’ is an economic slowdown that avoids recession.

xviii - FactSet

xix - FactSet

xx - All GDP growth estimates from FactSet, July 5, 2023

xxi - All U.S. treasury yield information from FactSet

xxii - Strategas

xxiii - FactSet, Washington Trust calculations

xxiv - FactSet

Connect with a wealth advisor

No matter where you are in life, we can help. Get started with one of our experts today. Contact us at 800-582-1076 or submit an online form.

This document is intended as a broad overview of some of the services provided to certain types of Washington Trust Wealth Management clients. This material is presented solely for informational purposes, and nothing herein constitutes investment, legal, accounting, actuarial or tax advice. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. Please consult with a financial counselor, an attorney or tax professional regarding your specific financial, legal or tax situation. No recommendation or advice is being given in this presentation as to whether any investment or fund is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors, or markets identified and described were, or will be, profitable.

Any views or opinions expressed are those of Washington Trust Wealth Management and are subject to change based on product changes, market, and other conditions. All information is current as of the date of this material and is subject to change without notice. This document, and the information contained herein, is not, and does not constitute, a public or retail offer to buy, sell, or hold a security or a public or retail solicitation of an offer to buy, sell, or hold, any fund, units or shares of any fund, security or other instrument, or to participate in any investment strategy, or an offer to render any wealth management services. Past Performance is No Guarantee of Future Results.

It is important to remember that investing entails risk. Stock markets and investments in individual stocks are volatile and can decline significantly in response to issuer, market, economic, political, regulatory, geopolitical, and other conditions. Investments in foreign markets through issuers or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, or other conditions. Emerging markets can have less market structure, depth, and regulatory oversight and greater political, social, and economic instability than developed markets. Fixed Income investments, including floating rate bonds, involve risks such as interest rate risk, credit risk and market risk, including the possible loss of principal. Interest rate risk is the risk that interest rates will rise, causing bond prices to fall. The value of a portfolio will fluctuate based on market conditions and the value of the underlying securities. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment loss. Investors should contact a tax advisor regarding the suitability of tax-exempt investments in their portfolio.