Q1 Economic and Financial Market Outlook

January 17, 2024

By: Peter R. Phillips, CFA®, CAIA®

Senior Vice President and Chief Investment Officer

Washington Trust Wealth Management

2023 Recap: The Recession That Wasn’t

Despite multiple indicators and headwinds, the U.S. economy avoided recession in 2023, confounding many forecasters who predicted one with high confidence (us included). Indicators such as an inverted yield curve, a soft Institute for Supply Management (ISM) survey and tightening bank lending standards; and headwinds including the fastest and largest Fed Funds rate increase since 1980,[i] three of the largest bank failures in U.S. history,[ii] and two major global conflicts with the Russian-Ukrainian and Israeli-Hamas wars; all suggested economic slowdown and recession.

Instead, we experienced a surprisingly strong year for both the economy and financial markets. In fact, 2023 U.S. GDP growth is estimated to reach 2.4%, up from a meager 0.3% estimate at the beginning of the year.[iii] This unanticipated economic strength was supported by:

- A robust labor market. Despite heightened recession risks entering the year and some high-profile layoff announcements, the U.S. economy continued to be a job creation machine, adding approximately 2.7 million jobs in 2023, on top of 4.8 million in 2022 and 7.3 million in 2021. The 3.7% unemployment rate, while up from 3.4% earlier in the year, is at a historically low level.[iv]

- Solid wage gains, with real (adjusted for inflation) disposable personal income growth of over 4.0%.[v]

- Fiscal stimulus from multiple federal and state programs providing funding and tax relief, including remaining excess savings from earlier COVID-19 relief disbursements, student loan debt repayment suspension/forgiveness, American Rescue Plan Act (ARPA) spending, and Inflation Reduction Act (IRA) spending, among others.

2023 Financial Markets

Financial markets also posted strong gains, with the S&P 500’s year-end closing price just 0.5% shy of a record high.[vi] To be sure, it was a volatile year for both the equity and fixed income markets, but the year closed out with a powerful November/December market rally supported by moderating and better than expected inflation trends, a still robust economy, and signals from the Fed that a shift to more dovish/accommodative policy is near.

Essentially, the market consensus view declared victory for the Fed in its battle over inflation and switched towards an economic “soft landing” scenario.[vii] The Fed won!

Essentially, the market consensus view declared victory for the Fed in its battle over inflation and switched towards an economic “soft-landing” scenario.

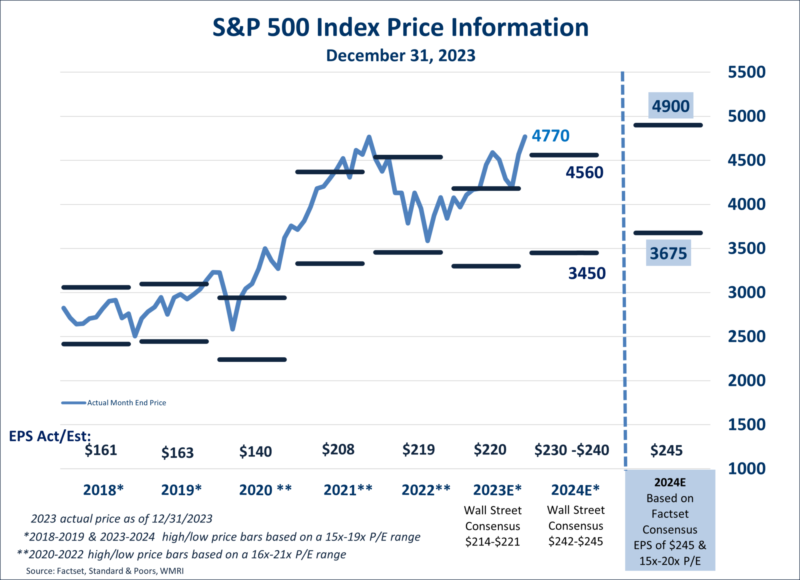

The S&P 500 returned 11.7% in Q4 and ended the year up 26.3% on a total-return basis. It’s important to note that the “Magnificent Seven” (Amazon, Apple, Google, Meta, Microsoft, Nvidia, and Tesla) were responsible for driving a good portion (approximately 60%) of that return. The median return for the Magnificent Seven was 80.9%, versus only 11.8% for the rest of the S&P 500.[viii]

Meanwhile, the Bloomberg U.S. Aggregate Bond Index[ix] returned 6.8% in Q4 and ended the year up 5.5% on a total-return basis. Interest rates/yields fell sharply in Q4, reflecting the market’s perceived victory over inflation and the prospects of a Fed pivot to more accommodative monetary policy and Fed funds rate decreases in 2024. (A fall in yields drives bonds prices—and total returns—higher.)

Both investment and non-investment grade (high-yield) corporate bonds delivered among the best returns in fixed income—8.5% and 13.4%, respectively—as credit spreads tightened, reflecting the relatively strong performance of the U.S. economy.

2024 Outlook: A Soft Landing

As strong as indicators were for a recession in 2023, they are now pointing towards an economic “soft landing” in 2024, even though an economic slowdown is still expected in the quarters ahead. [x]

“What we’re seeing now I think we can describe as a soft landing, and my hope is that it will continue.” - Treasury Secretary Janet L. Yellen, January 5, 2024 [xi]

Growth Estimates

At the beginning of 2023, the FactSet consensus 2023 U.S. Gross Domestic Product (GDP) growth estimate was 0.3%, and probability of recession was perceived to be high. The 2023 GDP estimate steadily increased through 2023 and recession timing was pushed out to 2024. We ended the year with a 2023 U.S. GDP growth estimate of 2.4% (we will get the first official measure of full year 2023 growth on January 25), which is a relatively respectable and higher-than-average growth rate over the past 15 years, and the viewpoint that recession risk in 2024 has been significantly reduced.

In fact, the consensus economic viewpoint now appears to call for an economic soft-landing. The FactSet consensus 2024 U.S. GDP growth estimate is now 1.2%, up from a low of 0.6% estimate six months ago[xii]; and importantly, on a quarterly basis estimates do not call for any negative growth quarters (while not the official definition of a recession, one indicator of recession is two consecutive quarters of negative GDP growth).

Fed Impact

Key to this soft landing viewpoint is the expectation that the Fed is done with rate increases and will pivot to a more accommodative policy stance in early 2024.

- The Fed’s preferred inflation measure, the “core” Personal Consumption Expenditures (PCE) Price Index (excluding food and energy prices), is closing in on the Fed’s 2% target. While the “core” PCE Price Index is at 3.1% on a year-over-year basis (down from a high of 5.6% in early 2022), the recent three-month annualized rate of change was 2.2%, close to the Fed’s target and continuing a downward trajectory.[xiii]

- The Fed signaled rate cuts in 2024. While future policy changes are uncertain and will be data dependent, the Fed’s own updated projections (the Fed dot plot) from the December 2023 meeting call for approximately 75 bps (basis points) of rate cuts in 2024.[xiv]

- The Fed funds futures market is anticipating 150 bps of rate cuts in 2024, starting as early as March. [xv] In our viewpoint, 150 bps of rates cuts seems a bit aggressive and likely implies sharper than anticipated drops in inflation and/or a sharper than anticipated slowdown in economic activity—each of which may have other consequences for the economy and financial markets.

Economic Growth Momentum

Positive economic growth momentum from 2023 has a better chance of carrying into 2024 with the Fed’s pivot to a more accommodative monetary policy position.

- The U.S. labor market continues to generate strong new job growth. The economy continues to add jobs at a respectable rate and job openings of 8.8 million, while down from a peak of 12 million early last year, is still a relatively large number and greater than the number of unemployed of 6.3 million.[xvi] The four-week moving average of weekly unemployment claims of approximately 208,000 is a relatively low number, historically, and suggests employers are continuing to hold on to their employees. The 3.7% unemployment rate, while up from 3.4% earlier in the year, is at a historically low level.[xvii]

- The strong employment landscape provides support for continued good personal income gains. Real (after adjustments for inflation) disposable personal income is improving and grew at a relatively robust 4.0% over the past year.[xviii]

- Good personal income gains supports continued consumer spending. Real personal consumption expenditures are growing at a relatively solid 2.7% year/year pace.[xix]

Of course, the projected lower interest rate environment, if it materializes, could help to invigorate multiple areas of the economy that have experienced weakness, including:

- Housing – Lower interest and mortgage rates could help the somewhat stalled housing market, where mortgage applications and existing home sales are at or below levels experienced during the Great Financial Crisis of 2007-2008.[xx]

- Capital Expenditures – While business capital spending has held steady; the outlook has deteriorated due to higher interest rates and tighter bank lending standards.[xxi]

- Banking Industry – Lower short-term rates (which are most sensitive to the Fed funds rate) could help normalize the yield curve (i.e., short-term interest rates being lower than longer-term rates) and improve bank earnings and lending capacity.

And lest we forget—2024 is an election year. Political observers would note that no first-term president since William McKinley has won reelection while the economy was in a recession during the last two years of his term.[xxii] As such, there is incentive for Washington to find ways to stimulate the economy should economic growth start to falter.

Reason for Caution

We certainly hold out hope for a soft landing in 2024, acknowledging the strong performance of the U.S. economy in 2023, as well as the significance of the Fed’s potential pivot to more accommodative monetary policy in 2024. However, we must acknowledge that several risks remain, and we continue to hold a cautious view on economic growth in 2024.

Fed’s Restrictive Monetary Policy

First and foremost, we must recognize the Fed’s restrictive monetary policy stance since March 2022. So far, that policy has created 525 bps of increases—the largest and fastest rate increase since 1980. The impact of monetary policy involves “long and variable lags” that can take nine to 24 months to impact the economy.[xxiii] This impact may still be felt long after the Fed has finished raising rates and starts cutting sometime in 2024. It is important to note that past Fed fund rate increase cycles have typically led to a slowdown in economic growth and often recession.

The impact of monetary policy involves “long and variable lags” that can take nine to 24 months to impact the economy.

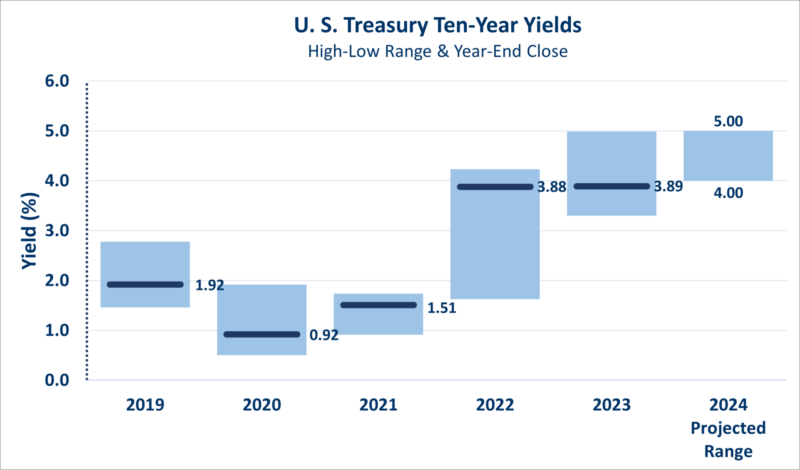

Inverted U.S. Treasury Yield Curve

An inverted U.S. Treasury yield curve has historically been a very good indicator of recession. Both the 2y–10y U.S. Treasury spread and 3m–10y U.S. Treasury spread continue to be inverted as of December 31, 2023, at -37 bps and -147 bps, respectively—and have been for an extended period. The Federal Reserve Bank of New York’s recession probability indicator, based on U.S. Treasury yield spreads, puts the probability of recession within the next twelve months at 63%.[xxiv]

Banking Industry Challenges

Challenging operating conditions in the banking industry remain a concern.[xxv] Although fallout from bank failures in early 2023 have been contained, and the country’s largest banks appear sufficiently capitalized,[xxvi] operating conditions remain a challenge for the industry.

Deposit outflows appear to have stabilized, but higher yielding competing products may continue to draw deposits out of the banking system; and deposit costs continue to increase, negatively impacting profitability. Additionally, banks continue to hold significant unrealized investment losses in their investment securities portfolios.

The combination of higher borrowing costs and reduced liquidity could serve to further tighten bank lending standards, which are already at levels historically associated with economic slowdown and recession.[xxvii]

U.S. Government Fiscal Health

We are also concerned about the U.S. Government’s fiscal condition and its potential to negatively impact government spending and tax policy, and in turn economic growth, in the years to come. The gross debt of the United States Government has grown $10.8 trillion, or 46%, since the end of 2019 (just before the pandemic)—and now stands at $34.0 trillion (as of 12/29/23).[xxviii] Due to the significantly higher debt levels and the sharp rise in interest rates over the past year, the Congressional Budget Office (CBO) estimates that net interest payment on the nation’s debt (or the cost to just service the debt) will rise to over 15% of total government revenue by 2025, up from 9.7% in 2022, and an average of 8.7% from 2013-2022.

This has significant implications for government spending and tax policy in the years to come, especially given the U.S. budget already operates in a deficit, which the CBO estimates to be approximately 17% of revenue in 2024, excluding interest payments.[xxix]

Further, the recent political upheaval related to passing annual appropriations bills and the resulting removal of the Speaker of the House highlight the increasingly volatile political environment and heightens risk.

Other Economic Indicators

Various other economic indicators also suggest caution is warranted. The Conference Board Leading Economic Index (LEI), which includes ten components across financial, labor, manufacturing, consumer and housing markets, has declined in each of the last seventeen months and is at a level that signals recession within the next 12 months.[xxx] The ISM index of manufacturing activity remains at and has been at a level that suggests economic contraction since late 2022, with the new orders and backlog components of the index especially weak.[xxxi] Consumer confidence levels, specifically the future expectations component, is at a level typically associated with recession.[xxxii]

Financial Markets

While the economic outlook has improved, we hesitate to give the “all clear” for the financial markets. A strong stock market performance in 2023 seems to indicate clarity on the economy (soft-landing), Fed policy (lower interest rates), and corporate earnings (double-digit growth). However, we think some caution is reasonable.

Fixed Income

We continue to see opportunity to extend duration and potentially lock-in higher yields for the longer-term. Moderating inflation trends towards the Fed’s 2% target and the Fed’s projection of Fed funds cuts in 2024 sent yields sharply lower in the last quarter of 2023; however, yields are still on the higher end of the 15 year range.

Yields. The 2-year Treasury ended the year yielding 4.25%, down sharply from the 5.21% peak in mid-October and down from 4.42% at the beginning of the year, but still at the high-end of the 15-year range of 0.09%-5.21%. The 10-year Treasury ended the year yielding 3.88%, down sharply from the 4.99% peak in mid-October and at the same level as the beginning of the year, but still at the high-end of the 15-year range of 0.50%-4.99%.[xxxiii]

Another year of stronger-than-expected economic growth and/or inflation resurgence could reverse current sentiment and push rates higher, hurting fixed income total returns. However, based on consensus forecasts, it could be that we have already witnessed peak yields for this cycle. Further, should the economy slow more than expected and/or recession develop, the Fed may need to be more aggressive with rate cuts and lower yields across fixed income markets and enhancing fixed income total returns.

Portfolio Duration. We continue to see opportunity to extend portfolio duration and lock in some higher yields for the longer-term. Current high money market yields are likely to fall should the Fed pause and pivot. Timing the exact inflection point of peak yields is probably not the best investment strategy.

Credit spreads. Credit spreads are at the low end of historical ranges and do not appear to price in any hiccups in the economy—and especially not any significant slowdown and/or recession; therefore, it may be too early to add exposure to lower quality corporate bonds. Investment grade spreads at 99 bps remain slightly below the twenty-year average of about 149 bps and significantly below spreads during economic slowdowns and recessions. High Yield spreads at 323 bps remain significantly below the twenty-year average of about 494 bps, and significantly below spreads during economic slowdowns and recessions.

Equity

We continue to have a cautious outlook for stock prices. While higher stock prices are always welcome, stocks do not appear “cheap” and seem to leave little room for any disappointing news.

Corporate Earnings. Current consensus S&P 500 earnings call for 2024 earnings growth to accelerate to 11.4%, up from an estimated 0.1% growth in 2023; however, consensus economic forecasts call for a slowdown in GDP growth. Earnings growth of 11.4% may prove to be a bit too optimistic for a slowing economy.[xxxiv]

Valuation. The recent rally in stock prices has driven the S&P 500’s price/earnings ratio (valuation) to a relatively expensive level. The rally in stock prices puts the current S&P 500 p/e ratio based on 2024 estimates at 19.5x. This is not a cheap valuation, especially in a still heightened inflationary and interest rate environment. If inflation and interest rates fail to fall in the coming year, then we see a downside risk to valuation. (There is an inverse correlation between inflation and p/e ratios. Higher inflationary environments typically result in lower p/e ratios.)

Current valuation levels leave little room for any disappointment, whether it be from the economy, corporate earnings, or some other unforeseen risk.

International Equity. We continue to underweight our exposure to international equities but see performance benefits from a weak U.S. dollar. Although valuations appear significantly lower than in the U.S., earnings growth rates across the developed international countries are much less attractive, partly due to their more modest exposure to global scale information and medical technology companies.

In addition, the Russian/Ukraine conflict has a much greater and direct impact on economies across Europe. Recession risk is elevated across Europe. In the emerging markets, heightened risks keep us cautious—specifically, geopolitical risks related to China.

We do recognize a weaker U.S. dollar will boost unhedged international investment returns. The U.S. dollar fell 3.5% versus the Euro in 2023, and the consensus forecasts call for further dollar weakness in anticipation of lower U.S. inflation, a more accommodative U.S. Federal Reserve policy, and improving global economic growth relative to the U.S.[xxxv] As such, we do see value in having some exposure to international equities.

A Final Word

The twists and turns of 2023 reinforce the importance of focusing on a long-term financial plan and investment strategy. Reacting to a recession forecast, bank failures, major global conflicts, and a debt ceiling crisis could lead investors to deviate from a long-term financial plan and asset allocation decisions—particularly to allocate capital to risk assets. However, as we have witnessed in the past, such events may not end up having significant impact on long-term investment returns.

This is a reminder that while short-to-medium term forecasts should help inform decisions on near-term liquidity needs and availability, they should only have a minimal impact on a long-term asset allocation investment strategy. As we have seen time and time again, market-timing is difficult and can compromise long-term investment performance.

As we start the new year, it may be a good time to speak with your portfolio manager/investment advisor and review your investment objectives and asset allocation.

1 “Fed’s interest rate history” Bankrate, December 2023

2 Wikipedia. https://en.wikipedia.org/wiki/List_of_largest_bank_failures_in_the_United_States

3 FactSet

4 Employment statistics from FactSet

5 FactSet

6 FactSet

7 An economic ‘soft landing’ is an economic slowdown that avoids recession.

8 S&P and individual stock performance statistics from FactSet and WTWM calculations

9 The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar- denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, fixed- rate agency MBS, ABS and CMBS (agency and non-agency)

10 An economic ‘soft landing’ is an economic slowdown that avoids recession.

11 “Treasury secretary on economy: Pessimism has proven unwarranted” https://www.youtube.com/watch?v=SY65T7uruzE CNN, January 5, 2024

12 All GDP growth estimates from FactSet as of January 8, 2024

13 Factset, PCE Price Index as of November 2023

14 FOMC Summary of Economic Projections, December 2023

15 CME Fed Watch Tool as of January 8, 2024

16 FactSet

17 Employment statistics from FactSet

18 FactSet

19 FactSet

20 FactSet

21 FactSet

22 “All the U.S. Presidents Who Won Re-Elections During a Recession” Newsweek, March 20, 2020

23 Federal Reserve Bank of St. Louis, “Examining Long and Variable Lags in Monetary Policy’, Bill Dupor, May 24, 2023.

24 FactSet, Federal Reserve Bank of New York

25 Bank industry data from the FDIC Quarterly Banking Profile, Second Quarter 2023,

26 Board of Governors of the Federal Reserve System, 2023 Federal Stress Test Results, June 2023

27 FactSet, Federal Reserve, October 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices

28 U.S Department of the Treasury. Fiscaldata.treasury.gov

29 Congressional Budget Office. An Update to the Budget Outlook: 2023 to 2033, May 2023

30 The Conference Board, US Leading Indicators press release, December 21, 2023

31 FactSet

32 FactSet

33 FactSet

34 Earnings estimate data from FactSet

35 FactSet

Connect with a wealth advisor

No matter where you are in life, we can help. Get started with one of our experts today. Contact us at 800-582-1076 or submit an online form.

By accessing the noted link you will be leaving Washington Trust's website and entering a website hosted by another party. Washington Trust is not responsible for, nor do we control, endorse or guarantee the content of any external sites. Please be advised that you will no longer be subject to, or under the protection of, the privacy and security policies of Washington Trust's website. We encourage you to read and evaluate the privacy and security policies of the site you are entering, which may be different than those of Washington Trust.

By accessing the noted link you will be leaving Washington Trust's website and entering a website hosted by another party. Washington Trust is not responsible for, nor do we control, endorse or guarantee the content of any external sites. Please be advised that you will no longer be subject to, or under the protection of, the privacy and security policies of Washington Trust's website. We encourage you to read and evaluate the privacy and security policies of the site you are entering, which may be different than those of Washington Trust.

By accessing the noted link you will be leaving Washington Trust's website and entering a website hosted by another party. Washington Trust is not responsible for, nor do we control, endorse or guarantee the content of any external sites. Please be advised that you will no longer be subject to, or under the protection of, the privacy and security policies of Washington Trust's website. We encourage you to read and evaluate the privacy and security policies of the site you are entering, which may be different than those of Washington Trust.

By accessing the noted link you will be leaving Washington Trust's website and entering a website hosted by another party. Washington Trust is not responsible for, nor do we control, endorse or guarantee the content of any external sites. Please be advised that you will no longer be subject to, or under the protection of, the privacy and security policies of Washington Trust's website. We encourage you to read and evaluate the privacy and security policies of the site you are entering, which may be different than those of Washington Trust.

This document is intended as a broad overview of some of the services provided to certain types of Washington Trust Wealth Management clients. This material is presented solely for informational purposes, and nothing herein constitutes investment, legal, accounting, actuarial or tax advice. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. Please consult with a financial counselor, an attorney or tax professional regarding your specific financial, legal or tax situation. No recommendation or advice is being given in this presentation as to whether any investment or fund is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors, or markets identified and described were, or will be, profitable.

Any views or opinions expressed are those of Washington Trust Wealth Management and are subject to change based on product changes, market, and other conditions. All information is current as of the date of this material and is subject to change without notice. This document, and the information contained herein, is not, and does not constitute, a public or retail offer to buy, sell, or hold a security or a public or retail solicitation of an offer to buy, sell, or hold, any fund, units or shares of any fund, security or other instrument, or to participate in any investment strategy, or an offer to render any wealth management services. Past Performance is No Guarantee of Future Results.

It is important to remember that investing entails risk. Stock markets and investments in individual stocks are volatile and can decline significantly in response to issuer, market, economic, political, regulatory, geopolitical, and other conditions. Investments in foreign markets through issuers or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, or other conditions. Emerging markets can have less market structure, depth, and regulatory oversight and greater political, social, and economic instability than developed markets. Fixed Income investments, including floating rate bonds, involve risks such as interest rate risk, credit risk and market risk, including the possible loss of principal. Interest rate risk is the risk that interest rates will rise, causing bond prices to fall. The value of a portfolio will fluctuate based on market conditions and the value of the underlying securities. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment loss. Investors should contact a tax advisor regarding the suitability of tax-exempt investments in their portfolio.