Economic and Financial Market Outlook

April 20, 2022

The global and U.S. economies are facing significant headwinds this year. As a result, the consensus estimates of leading economists for U.S. GDP growth in 2022 has dropped to 3.4%, down from 4% at the beginning of the year[i]. Nonetheless, we still expect 2022 to rank among the top years of the last 20, an extended period when the median annual GDP growth rate in the U.S. was a relatively sluggish 2.3%[ii].

The latest International Monetary Fund (IMF) 2022 Global GDP forecast is 4.4%[iii].That estimate is from January 2022 -- prior to the Russian invasion of Ukraine, additional elevated inflation readings, and more aggressive U.S. Fed tightening expectations. When the IMF updates its forecast in mid-April, we expect estimates to move materially lower.

Headwinds Dominate the Headlines:

The Ukraine Fallout

Fallout from Russia’s unexpected and shocking invasion of Ukraine is reverberating throughout the global economy. While neither Russia nor Ukraine are large components of global GDP, both countries are important producers and exporters of energy and grains, especially to Europe. Production disruptions and sanctions are exacerbating pressures on global supply chains and driving spikes in inflation, especially in energy and food commodities across the world.

Unfortunately, an end to the war does not appear close as Russian forces regroup for a new wave of attacks in the east of the country. Significant risk also remains that the conflict escalates beyond the borders of Ukraine entangling other nations and even engaging NATO. Such a scenario would certainly worsen the humanitarian crisis and have a decidedly negative impact on the world economy and financial markets.

Inflation at Historic Highs

At 7.9%, inflation is at a 40-year high and threatens the sustainability of the current economic recovery.[iv] Inflation rates have risen across most areas of the economy and may soon start to impact consumer spending decisions.

Oil & gasoline prices, in particular, have increased about 80%over the past year. [v]This represents a significant ‘tax’ on consumers’ income and reduces the income available for discretionary spending. Also, historically, such large and sustained increases in energy prices typically lead to a slowdown in GDP growth.

Rates are Rising

The U.S. Federal Reserve is expected to take an aggressive approach towards battling inflation by increasing the Fed funds rate and reducing the size of its balance sheet. The Fed funds rate started the year at 0.0%-.25% and now the Fed funds futures market expects the Fed funds rate to end the year in a range of 2.5%-3.0%[vi]. Some Fed governors are also signaling the need for a ‘rapid’ reduction of the Fed’s balance sheet (i.e., the sale of the Fed’s fixed income holdings – or quantitative tightening).

Both actions from the Fed are likely to put upward pressure on interest rates throughout the economy making it more costly for businesses and consumers to borrow money, which in turn may slow economic growth.

Despite the Headwinds, the U.S. Economy Remains Strong

The U.S. labor market remains healthy and further improvement is possible. The U.S. economy gained approximately 6.7 million jobs in 2021 and an additional 1.7 million jobs in the first three months of 2022. The unemployment rate now stands at 3.6%, a historically low level and close to the pre-pandemic low[vii].

Extended COVID-related unemployment benefits from the Federal government have ended and this appears to have encouraged more people to enter or re-enter the job market. Since December, the civilian labor force has increased by 2.1 million resulting in a labor force participation rate of 62.4%, up from 61.9% -- but still below the pre-pandemic level of 63.4%[viii].

It appears there is room for additional recovery in the labor market, which bodes well for continued economic momentum into 2022. Personal spending also remains healthy (up over 13% on a year-over-year basis) and strong across most areas of the economy[ix]. Housing market activity continues to be robust. The recent sharp increase in mortgage rates presents a headwind but low housing inventory may help keep supply/demand in balance and provide stability.

Finally, despite the sharp increase in nominal interest rates, real yields remain negative and accommodative for growth. The real Fed funds rate (adjusted for inflation) is approximately -6.0%, close to the lowest level in 50 years[x].

The State of the Financial Markets: More of the Same

Fixed Income

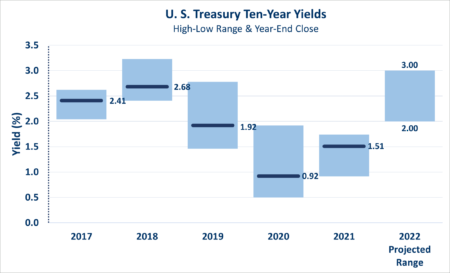

The Bloomberg Aggregate Bond Index declined 5.9% (including income) in the first quarter of 2022, the worst quarterly performance for the U.S. bond market in over 40 years [xi]. As interest rates spiked in response to inflation and changes in Fed policy, bond prices fell.

We expect interest rates will continue to move higher as the Fed begins to tighten monetary policy.

Short-term The recent and sharp rise in short-term rates may already fully reflect expected Fed moves through 2022. In fact, the 2-year Treasury is closing in on a 10-year high[xii].

Long-term We expect longer-term yields to continue to move higher in 2022 driven by both inflation and the Fed’s efforts to reduce the size of its balance sheet (quantitative tightening). The CPI, a measure of inflation, is currently at 6.4% on a y/y basis (the highest reading in 40 years), making 10-year ‘real’ yields significantly negative[xiii]. We would not expect such extreme negative real yields to persist for an extended period, especially given the now dismissed viewpoint that current inflation levels are merely transitory.

We continue to prefer shorter duration, high quality fixed income exposure to protect from an increase in interest rates and a widening of credit spreads.

In the mortgage and asset-backed segment of the bond market, the end of the Fed’s bond buying program could negatively impact spread pricing. As such, we remain a bit wary of this segment of the fixed income market. We are wary as well of Investment Grade and High Yield Corporates where spreads are well below their 25-year averages[xiv] and may not provide adequate compensation for the inherent credit risk.

On a positive note, nominal yields on shorter maturities are now approaching 10-year highs[xv] and are significantly more attractive as investments than just a few months ago. In addition, yields on money market funds are now above zero, allowing investors to nominally earn something on cash balances. Yields on longer-dated maturities have also become a bit more attractive on a nominal basis but still appear rich when adjusted for inflation.

Equities

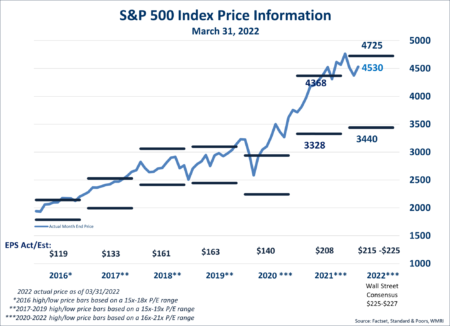

Underlying corporate earnings remain supportive of stock prices, but inflation and Fed action could negatively impact both earnings growth and stock valuations.

We expect S&P 500 earnings per share to grow at a mid-to-high single digit rate in 2022 driven by the still solid underlying economic environment. However, we are monitoring the impact of inflation, with specific attention to tight labor market conditions and resulting wage gains on corporate profitability. Also, the Fed’s aggressive tightening actions could slow economic activity resulting in weaker than expected corporate sales and earnings growth.

Higher inflation and interest rates favor Value over Growth stocks. We have seen some rotation out of high growth and speculative stocks into stocks with higher quality fundamentals and more modest valuations.

Our preference is to be long-term equity investors and therefore have a bias towards high quality companies with long-term secular and/or dividend growth potential. This ‘growth’ component of our equity strategy preference may be challenged in the short-term, but we believe is appropriate for the long-term.

We continue to underweight our exposure to international equities. Although valuations appear lower than in the U.S., earnings growth rates across the developed international countries are much less attractive, partly due to their more modest exposure to global scale information and medical technology companies. In addition, the Russian/Ukraine conflict has a much greater and direct impact on economies across Europe.

In the emerging markets, heightened risks keep us cautious -- specifically the Chinese government’s recent regulatory crackdown on large information technology companies.

Overall, we have a cautious view on near-term stock market performance. We expect some slowdown in earnings growth and see risk to the current valuation level. Volatility may stay elevated due the conflict in Ukraine and the expected, but still uncertain, actions from the Fed. Nevertheless, the still low interest rate environment and a lack of attractive investment alternatives may provide near-term support for stock prices.

[i] Factset

[ii] Factset

[iii] World Economic Outlook Update, January 2022, IMF, January 25, 2022

[iv] Factset, CPI reading as of February 2022, April 11, 2022

[v] Factset. One year price change of the rolling 12-month average spot price of WTI oil and Regular Gasoline NY Harbor as of March 31, 2022

[vi] CME FedWatch Tool, Countdown to FOMC: CME FedWatch Tool (cmegroup.com), April 11, 2022

[vii] Factset

[viii] Factset

[ix] Factset

[x] Factset

[xi] Factset

[xii] Factset

[xiii] Factset, Core CPI reading as of February 2022, April 11, 2022

[xiv] Factset

[xv] Factset

__

Investments in foreign markets through issuers or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, or other conditions. Emerging markets can have less market structure, depth, and regulatory oversight and greater political, social, and economic instability than developed markets. Fixed Income investments, including floating rate bonds, involve risks such as interest rate risk, credit risk and market risk, including the possible loss of principal.

Interest rate risk is the risk that interest rates will rise, causing bond prices to fall. Past performance does not guarantee future results and the opinions presented cannot be viewed as an indicator of future performance. The S&P 500 Index is an unmanaged index and is widely regarded as the standard for measuring large-cap U.S. stock-market performance. In addition, the S&P 500 Index cannot be invested in directly and does not reflect any fees, expenses or sales charges. Further, such index includes 400 industrial firms, 40 financial stocks, 40 utilities and 20 transportation stocks. The information we provide does not constitute investment or tax advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell any security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Please consult with your Portfolio Manager, Financial Counselor, Relationship Manager, attorney or tax professional regarding your specific investment, legal or tax situation.

Connect with a wealth advisor

No matter where you are in life, we can help. Get started with one of our experts today. Contact us at 800-582-1076 or submit an online form.

By accessing the noted link you will be leaving Washington Trust's website and entering a website hosted by another party. Washington Trust is not responsible for, nor do we control, endorse or guarantee the content of any external sites. Please be advised that you will no longer be subject to, or under the protection of, the privacy and security policies of Washington Trust's website. We encourage you to read and evaluate the privacy and security policies of the site you are entering, which may be different than those of Washington Trust.

This document is intended as a broad overview of some of the services provided to certain types of Washington Trust Wealth Management clients. This material is presented solely for informational purposes, and nothing herein constitutes investment, legal, accounting, actuarial or tax advice. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. Please consult with a financial counselor, an attorney or tax professional regarding your specific financial, legal or tax situation. No recommendation or advice is being given in this presentation as to whether any investment or fund is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors, or markets identified and described were, or will be, profitable.

Any views or opinions expressed are those of Washington Trust Wealth Management and are subject to change based on product changes, market, and other conditions. All information is current as of the date of this material and is subject to change without notice. This document, and the information contained herein, is not, and does not constitute, a public or retail offer to buy, sell, or hold a security or a public or retail solicitation of an offer to buy, sell, or hold, any fund, units or shares of any fund, security or other instrument, or to participate in any investment strategy, or an offer to render any wealth management services. Past Performance is No Guarantee of Future Results.

It is important to remember that investing entails risk. Stock markets and investments in individual stocks are volatile and can decline significantly in response to issuer, market, economic, political, regulatory, geopolitical, and other conditions. Investments in foreign markets through issuers or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, or other conditions. Emerging markets can have less market structure, depth, and regulatory oversight and greater political, social, and economic instability than developed markets. Fixed Income investments, including floating rate bonds, involve risks such as interest rate risk, credit risk and market risk, including the possible loss of principal. Interest rate risk is the risk that interest rates will rise, causing bond prices to fall. The value of a portfolio will fluctuate based on market conditions and the value of the underlying securities. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment loss. Investors should contact a tax advisor regarding the suitability of tax-exempt investments in their portfolio.